- The Blockchain for Africa

- info@horizonafrica.io

Blockchain and FinTech in Mauritius

Photo by Edi Kurniawan on Unsplash

Fintech, financial technology for short, is the innovative use of technology to solve some financial use cases. The 3 main reasons behind the hype around fintech are the financial crisis of 2008, the wave of innovation that happened after that period, and the emergence of Satoshi's Bitcoin Blockchain. After the 2008 financial crisis, banks and financial institutions were busy dealing with the sanctions, fines, new regulations imposed on them by governments and innovation became a very distant priority.

Emergence of Fintech

At the same time, a new wave of innovation happened all around the world, including Mauritius, in the form of WhatsApp, Uber, AirBnb, Facebook and this has created a gap in what users came to expect from a user experience point of view and what banks were offering. That gap was so big that technology firms started to join the party. Facebook has more than 50 licenses in the US in regards to money transfer through Messenger. WhatsApp has already started money transfer in India. There are also other big players like Apple Pay and Amazon which are making tremendous strides in the Fintech sector. It could well happen that our children's first bank account will be with Facebook instead of a traditional bank. Banks should be worried. With more than 2 billion people unbanked in the world, those technology firms are also solving the problem of inclusion.

Mauritius has been at the forefront of this revolution with the establishment of the Mauritius Africa Fintech Hub (MAFH) and its members along with startups engaged in innovative projects including Horizon Africa and Demars. And then, there is the emergence of cryptocurrencies and blockchain-based systems.

The potential of Blockchain

People and experts from different sectors are pointing in a very specific direction when referring to the Blockchain technology and Cryptocurrencies. They claim that it could be as big as the Internet, literally calling it the new Internet, with the potential to radically change our lives and the way we communicate and interact not only with people around us, but with financial systems. In this state of things, there will be winners and losers, and innovation will mostly determine the outcome of most ventures.

What is Blockchain?

A lot of people define blockchain as the technology behind cryptocurrencies. An analogy for this definition would be to define the Internet as the technology behind emails. Although this is true, it does not provide the full scope of the possibilities in terms of innovation this new paradigm offers. One simple way to think of a blockchain is thinking about it as one big ledger. Ledgers currently form a very important part of our lives. They are owned by banks, financial regulators, routing banks, insurance companies and other third party entities. The current system causes a lot of friction in the way things work and the cost has to be ultimately borne by customers. This is where a blockchain-based decentralized system brings in a different way of doing things by reducing the load on different systems, reducing the role of intermediaries and ultimately reducing the cost of transactions.

A blockchain saves data in blocks which are linked to the next blocks. This effectively creates a chain of blocks of information where changing a prior information would require someone to change a bunch of other blocks, thereby increasing the security of the system. Information stored in blocks can be traced back based on the fact that the whole history of transactions is available.

Blockchain Networks

As mentioned earlier, a blockchain is based on a decentralized architecture. This, if not properly managed will create a chaotic system instead of the structured blockchain systems that we are currently familiar with. Miners form the crux of a blockchain network. A blockchain is all about transactions and there needs to be someone to take these transactions, validate them, and add them to blocks in a correct way. This is the role of miners. They sustain the day-to-day running of the network. Now, the question that comes to mind is why would a miner do this work for free? Well, they don’t. They get paid in terms of cryptocurrencies to do their work.

Imagine this: you have an open source, decentralized, peer-to-peer and trustless system. When you think about it, these are all ingredients to a chaotic recipe - where everyone will do what they want. You need to define rules in the network for all of these components to work correctly together. This is the role of consensus algorithms.

The different consensus algorithms define the way different blockchains work. As such, there are different blockchains available each with their own advantages and drawbacks:

- Everyone obviously knows about the bitcoin blockchain, which is basically a fully decentralized and trustless payment system.

- Ethereum is an open source, public and open blockchain. The main distinction between Ethereum and Bitcoin is the fact that Ethereum has been built to allow people and companies to build smart contracts. It is basically an operating system which allows you to build decentralized software.

- Ripple aims to replace SWIFT, the interbank message platform for money transfers. It is actually a settlement system, currency exchange and remittance network. Ripple is not a blockchain in the traditional sense but given its importance in the banking sector and its structure being kind of borrowed from a traditional blockchain, it is difficult to exclude Ripple from a blockchain discussion.

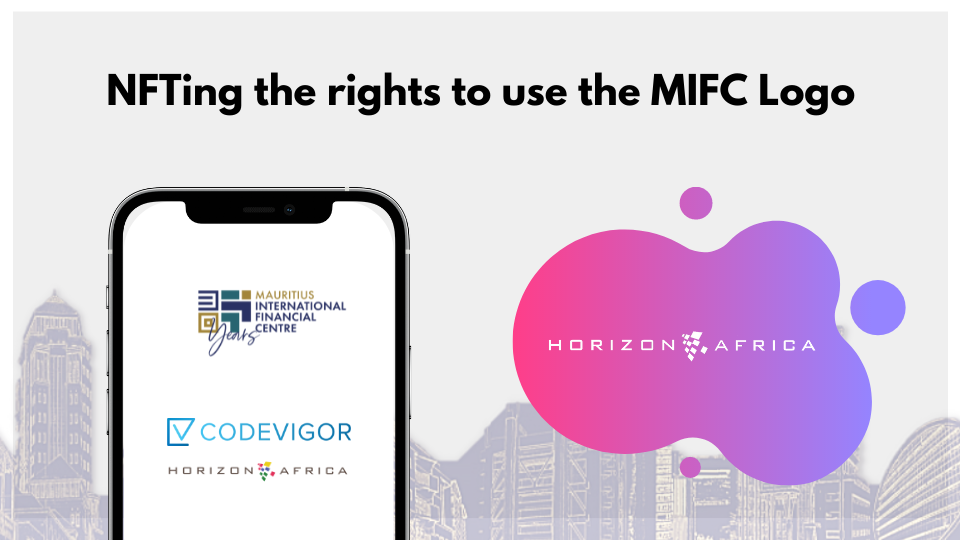

- Horizon Africa is a permissioned blockchain aimed at the African continent. The aim of Horizon Africa Blockchain is to allow Mauritian and other African companies to start using the blockchain technology in a concrete way. The mission is simple: analyse, build and deploy.

Blockchain and Fintech Use Cases

Some of the use cases that can be applied to the blockchain technology in Mauritius and other African countries include:

- Smart Contracts - smart contracts are programming constructs that allow things to get executed without any outside intervention. You define the rules, you define the inputs and you let the programming logic do the work automatically.

- Blockchain is a technology which allows you to reduce the importance and in some cases replace intermediaries. For example, to ensure that a transfer of Bitcoin or any other cryptocurrency has taken place, the public ledger acts as the middleman to verify transactions.

- Transactions - assigning ownership of assets.

- Fraud Detection - history tracking is very easy to do in a public ledger and the fact that transactions are immutable, records are much more reliable.

- Verification of information - or ensuring the integrity of information, be it in the form of documents, or digital assets.

Where to Start?

Any kind of use case requires a certain number of steps:

- Study and evaluate the processes in your business.

- Analyze how blockchain technology can improve processes in your current business - in some cases, how blockchain can introduce a new source of revenue or create a new revenue model.

- Come up with a working prototype or solution based on the analysis.

Irrespective of the use case or industry, these steps remain the same. Horizon Africa will help businesses in each of those steps, from the analysis part to the development and deployment phase.

{kind=link}